Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Effects of icosapent ethyl according to baseline residual risk in patients with atherosclerotic cardiovascular disease: results from REDUCE-IT

Pascal M Burger, MD, Deepak L Bhatt, MD, MPH, MBA, Jannick A N Dorresteijn, MD, PhD, Stefan Koudstaal, MD, PhD, Arend Mosterd, MD, PhD, Fabrice M A C Martens, MD, PhD, P Gabriel Steg, MD, Frank L J Visseren, MD, PhD for the REDUCE-IT Investigators

Conclusions In patients with ACS treated with PCI, ticagrelor is associated with significantly more repeat coronary revascularizations compared to prasugrel after 12 months, predominantly in remote coronary vessels.

However this was a post hoc study ...but gives the general idea

Note

Funding Acknowledgements: Type of funding sources: Public grant(s) – National budget only. Main funding source(s): German Center for Cardiovascular Research (DZHK),

North.With respect . You should know the answer to your question by now ( will a 227 patient Greek trial suffice ?) Maybe poster Laurent will be willing to spend some time explaining to you the importance of.... size of clinical trials , powering of clinical trials and P values .

Don't know North. It would have to be some profound noticeable effect for the researchers to delve into it, as the study protocol and goals don't encompass such:

"The proposed study is a proof-of-concept, randomized, placebo-controlled, double-blind, parallel-group clinical trial assessing the efficacy of 18 months of icosapent ethyl (IPE) therapy on magnetic resonance imaging (MRI), cerebrospinal fluid (CSF), and cognitive biomarkers for AD in 150 cognitively-healthy Veterans ages 50-75 years. The overarching goal of this trial is to assess whether icosapent ethyl beneficially affects intermediate physiological measures associated with onset of AD in order to evaluate whether larger, multi-site, longer-duration Alzheimer's prevention trials are warranted to assess more definitive clinical outcomes. The proposed study aims to: 1) investigate the effects of 18 months of IPE vs. placebo on regional cerebral blood flow as measured by arterial spin-labeling MRI; 2) determine the impact of 18 months of IPE vs. placebo on CSF biomarkers of AD pathology; and 3) evaluate the effects of 18 months of IPE vs. placebo on cognitive performance." https://www.clinicaltrials.gov/study/NCT02719327?cond=Alzheimer%20disease&intr=Icosapent%20Ethyl&rank=1&tab=history&a=16

NORTH, I take all that BACK.. I found this on an Univ. of Wisconsin Department of Radiology website:

"In addition, data collection from this trial will allow for exploration of the impact of previous TBI and/or PTSD on response to therapy. We hypothesize that in this population, IPE will beneficially affect mechanisms central to AD pathology by: 1) increasing rCBF within the sROI; 2) reducing CSF A-beta-42; and that these neurobiological changes will be associated with 3) an increased ADCS-PACC cognitive composite score. While recognizing that the proposed trial is not addressing all potential effects of IPE, such as changes in measures of inflammation or oxidative stress, we will store neuroimages and blood and CSF samples for future analyses of other potential mechanisms." https://radiology.wisc.edu/research-projects/brave-epa-brain-amyloid-and-vascular-effects-of-eicosapentaenoic-acid-epa-in-adults-at-risk-for-alzheimers-disease/

Wouldn’t the 227 patients Greek trial suffice? See CaptBeer’s post this evening. Does Greek population differ from populations of France or Germany significantly?

See 60 minutes tonight, CBS-TV at 7:00 pm. Reports veteran-acquired PTSD can be “contagious” in the sense that veteran brings back and repeatedly tells wife and child horrific stories of explosions wiping out comrades in same location near him. The wife becomes despondent herself in constant caring of a now suicidal husband. Much caring of both is now in the hands of older child…and the story continues with child also becoming depressed. This husband eventually recovers, finds a job, and is able to support the family. The wife and child are interviewed, and relate the above story.

I wonder whether investigators in the BRAVE trial are seeing signs of the above developments in the veteran population studied and interviewed. Are family members also interviewed?

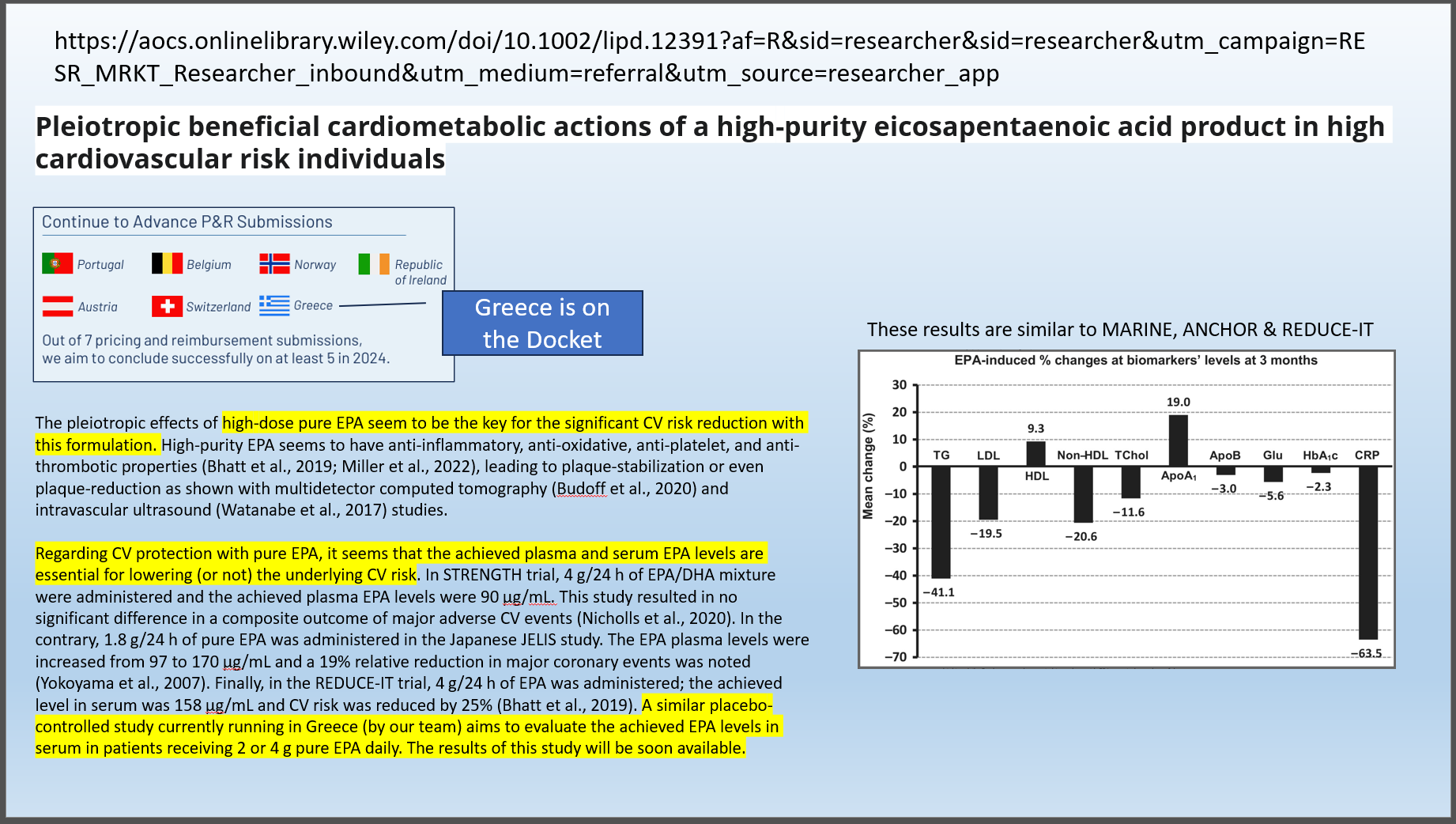

The article that I posted a few minutes ago describes a short biomarker study conducted in Greece similar in design to MARINE & ANCHOR. Several key biomarkers were significantly improved in a consistent dose dependent fashion like they did in MARINE/ANCHOR.

The authors have concluded that It’s the EPA Stupid and they are currently running a “placebo controlled” study which aims to evaluate EPA levels. They report that the results will be “available soon.”

BTW $AMRN has already submitted a dossier for approval in Greece.

Actually Monk I've been buying AMRN. Last purchase

Price. 0.8741

I figure I'll just tail alone on all the options handed out that vest next April at roughly that price...after this share buyback goes thru of course .

What better use of $50m then do buy back shares ( which should cause the remaining shares to go up in price ) so that the insiders ( and myself ) can make some $ here. Seems to be the current opinion anyway ...or at least what they have sold U on.

Of course if we really want to make some serious $ we need generous reimbursements in Germany , Italy and France ...and your ideas on how to achieve that ???? Please detail Thx Kiwi

North. Unless AMRN gets some relief from the courts in the US ( reversal of judge Du's decision , restraining generic infringement etc ) ...the US market is going nowhere. Break even at best because AMRN will be very unlikely to spend $ expanding this market .

So that leaves the EU where we now have patent protection until 2039 ( from memory ) One approach to gain access to Germany , Italy and France is to engage those Health Depts in a short trial for a specific sub group where the economic benefits of risk reduction can easily be quantified.

Consider that " out to lunch " if you like but in the mean time what your ideas for gaining market share in these 3 key EU markets ...the same ol same ol ? Kiwi

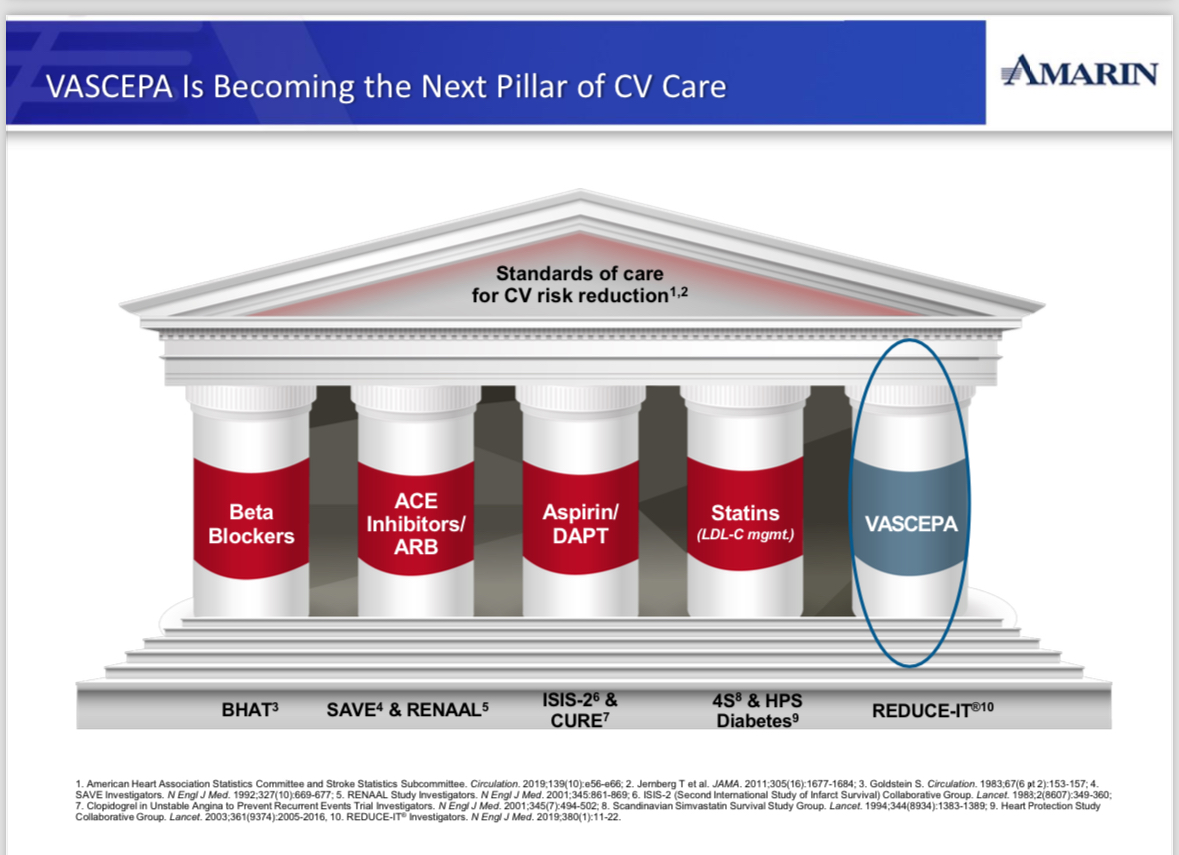

You are correct, and kiwi continues to be out to lunch in failing to acknowledge a line in one of DMC8’s links today that the Vascepa market is being retained because freedom from pancreatitis has not been shown by a generic clinical trial. The generics have the burden of proof.

Capt. I linked data from the supplemental section of the Revasc analysis but it didn't format easily ....If you look you will see a dramatic reduction in needing a repeat revascularisation for those on Vascepa Kiwi

The risk reduction ( and therefore potential cost savings ) in this subgroup is dramatic . The event lines separate very early and separation is very evident at the 3 yr pt. Yes we would need buy end to some extent from the Health Depts in Germany , France and Italy.

My understanding is that CAD patients are a lot more adherent to taking their meds after being admitted for a CV event . Recruiting should be a lot easier and quicker then R-IT since theres a lot of followup with these patients in the first months following a PCI

Capt. I was thinking of a short trial for a specific subgroup recruiting recent PCI patients in Germany , France and Italy. This would require the co operation of the health depts of those 3 countries . Say 1,000 patients in Germany with 500 each from France and Italy . . Unless theres a change in the US regarding generic infringement ...reversal of Judge Du's decision etc the US market is break even at best .

Because of the patent extension in the EU ...it's IMHO the only market we should spend $ developing at this time. To do that we need a buy in from the 3 major EU health dept markets mentioned above.

Why focus on Revasc rates following a PCI ? Because it's one of the sub groups with the largest risk reduction and the economic benefit of this risk reduction is easily quantified. Example ... assume there are 20,000 revasc cases following a PCI each year in Germany , Italy and France combined ...at an average cost 10,000 Euros each case ( less expensive then in the US ) = 200m Euros each year in cost to these 3 healthcare systems combined.

If SOC plus Vascepa reduces that event rate by 25% vs SOC alone in this patient population thats a savings of 50m Euro's . Would this 50m Euros savings cover the cost of providing all PCI patients with Vazkepa following their initial PCI procedure ? I don't know ...I'm just using this as an example of how AMRN could use a small focused trial like this to gain access to these markets ...assuming there was at least a 25% risk reduction in revasc rates

I'm not thinking of a rerun of the Reduce It trial . Simply a small focused trial in the 3 EU markets we need access to . JMO Kiwi

Obviously your post was to highlight the fact that Epadel in Japan maintained market share for a long time. Much of the stuff above is of course not very applicable now since the sales force was disbanded. If Amarin can hold onto sales in the U.S. (unfortunately it is a stagnant market) while conserving cash (other than share BB) long enough to get some traction in the EU, then there may be some hope staring us at the end of a very long dark tunnel.

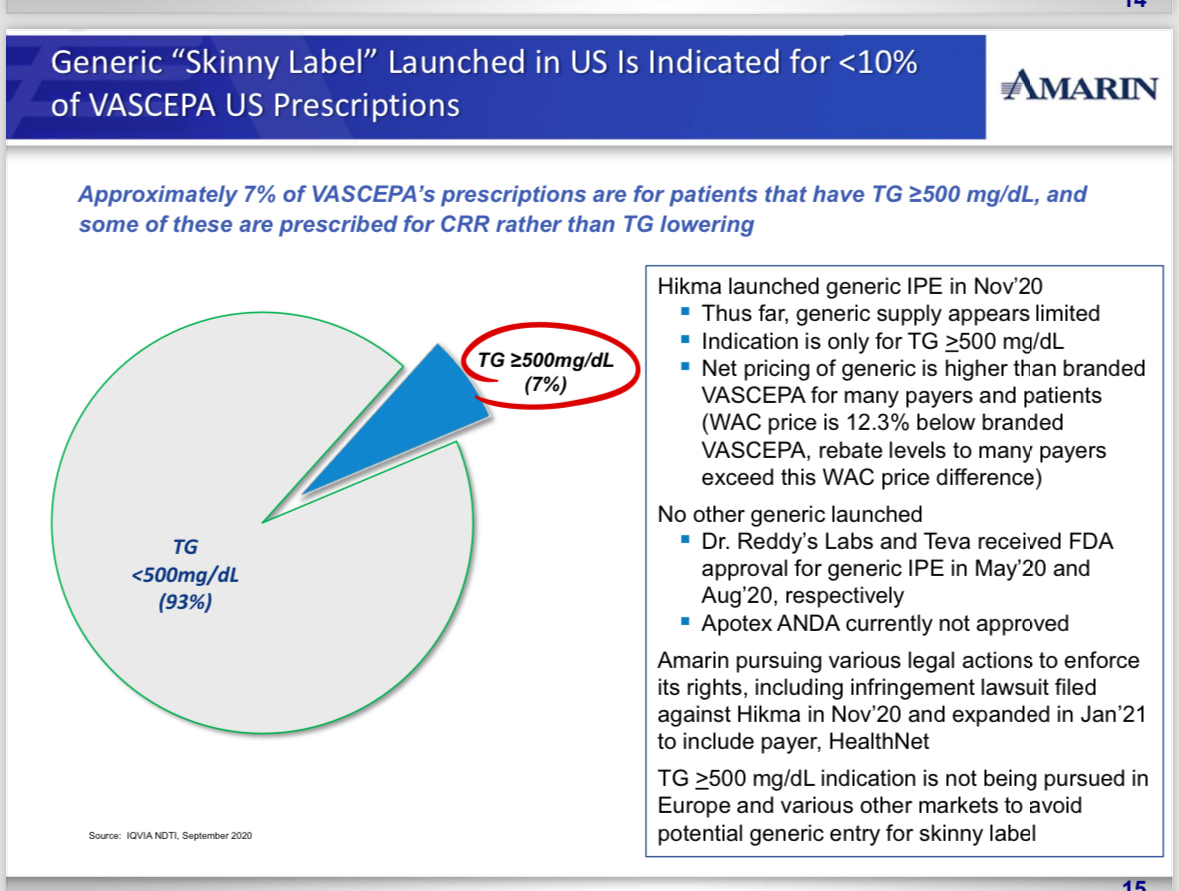

HIKMA/generics, can you also explain why you refused to state in your marketing statements that you have a generic version that can be used for the approved indication in the same fashion as the branded version?

Whale you pretend to be knowledgeable, you pretend to know medicine, you want to know everyone's business, your slippery comments about amrn are clearly negative. Rather than back up your stupid comments about share buybacks you go searching for anything else to avoid proving your lack of intelligence. Viet du caused amrn harm but at least stupid obese yanks have less access to Vascepa which their legal system caused. Is your wife still financially supporting you ??

RMB as a follow up re acquisitions . Acquisitions happen for several different reasons. Some Co's may have excellent P 2 trial results but are unable to fund a final pivotal trial(s ) needed for FDA approval or simply receive an offer to good to refuse from a larger Co. ...recent sales of Co's developing drugs for IgaN ( kidney disease ) for instance Other Co's like UNCY are not set up to launch the sales of their drug and will almost certainly look for a buyer if their final trial succeeds....same with TLPH . AMRN is an economies of scale situation ...as presented in Denners sales pitch . NVS has the economies of scale Kiwi

RMB. Denner's argument is economies of scale . A pervious poster had linked the pages in their presentation . NVS has economies of scale because they already have a sales force in the EU promoting Inclisiran ( their PCSK9 ) for CAD patients . IMHO the ideal combination for CAD patients is Inclisiran plus Vascepa .I wish Kaiser would allow me to do it .

Inclisiran is 3 shots for the first yr and 2 shots per year after that ...dramatically lowers LDL cholesterol ...done in a clinic. . First shot would be at annual physical so after that its just getting the patient back 6 mths later for their second shot . Likely far better adherence The problem with Statins is that roughly 50% drop them after the first year ( so adherence is poor ) and theres an increased risk for diabetes. PCSK9's like Repatha that I'm on ...require a trip to the hospital pharmacy once a month ( can't be shipped as its refrigerated ) and relies on my rather poor ability to self inject myself ( sub Q ) every 2 weeks.

So replace Statins and the other PCSK9's with Inclisiran and Vascepa ...both sold by NVS. . But NVS will want AMRN to get full EU reimbursement in place first ...which so far AMRN has failed to do .....and we await details on Wed as to any plans they may have in that area to be divulged .

Sure, there may not be any interest by any big EU Pharma but imo it would not necessarily be because of reimbursements, since there are many acquisitions made well before even drug approvals, never mind reimbursements.

Without such reimbursements in place I doubt any Big EU Pharma is interested/quote]

Sure, there may not be any interest by any big EU Pharma but imo it would not necessarily be because of reimbursements, since there are many acquisitions made well before even drug approvals, never mind reimbursements.

So AMRN sees no benefit in even doing a fairly short ...say 3 yr revascularisation trial like the following ..especially in light of the EU patent extension.

Drug-Coated Balloon (DCB) Angioplasty vs. Bare-Metal Stent (BMS) Implantation: A 6-month trial evaluating the clinical outcomes and restenosis rates between DCB angioplasty and BMS implantation in patients with de novo coronary lesions. Fractional Flow Reserve (FFR)-Guided PCI vs. Angiography-Guided PCI: A 3-month trial assessing the impact of FFR-guided PCI compared to angiography-guided PCI on long-term outcomes such as major adverse cardiac events (MACE) and target vessel revascularization (TVR). Bioresorbable Vascular Scaffold (BVS) vs. Drug-Eluting Stent (DES): A 1-year trial comparing the safety and efficacy of BVS with DES in patients undergoing percutaneous coronary intervention for stable angina or acute coronary syndrome.

Based on the graphs Laurent / Capt have posted , there should be very clear separation in event lines by 3 yrs , in revasc rates following a PCI between SOC and SOC plus Vascepa . There probably a lot of RWE data already on this waiting to be analyzed .

Whala, Always - for now years and years ALWAYS highlights barriers rather than opportunities.

Hard to understand what you are doing here (tens of thousands of posts) - always aiming to undermine trust in Amarin and Vascepa. ---------------------------------------

Please GO AWAY - and let the new BOD and MGT have the time it needs to turn this ship around !

Kiwi, I don't disagree that the Big 3 Euro countries are a problem. However, I don't see Amarin choosing to do any trials that would be "necessary" to approve V in these countries. It would take too long and be too costly. Not to mention, there is always the risk that something goes wrong with the trial.

I believe they will eventually succeed in Italy and France. But it will just take more time, and more data coordination (ie. RWE data, as well as additional R-It cohort analysis). I have no idea what will come of Germany. But in any event, I don't think additional trials will be the answer. So, I'm not sure where all this extra cash will be needed.

exwan…i need clarification…are you saying that the EU patent is for the “reduce-it” (heart) indication and therefore the coast is clear (i.e. the patent Wall is sound)?

No, there is no "same concern" in the EU as the Anchor patent has held and that is the only one that matters for the EU.

The issue in the US is that generics have been approved for the Marine indication as that patent has failed. That would be a minor issue if not for the fact that they are selling into the Anchor market. That still has a valid patent, but has been almost impossible to effectively enforce.

In the EU there is no Marine indication approved. Thus there are no Marine generics.

In theory somebody could run trials in the Marine indication in the EU and garner an approval for that. In reality that will never happen for economic reasons.

Irishpaddy ...well at least we have one thing in common .....I worked in sheep shearing gang in my youth . Hope U sold a big chunk of your AMRN after posting this Irishhpaddy

Re: jessellivermore post# 231436 Wednesday, December 04, 2019 11:45:04 AM Post# of 423606 JL

I am a sheep farmer scraping a living on the side of the Wicklow hills here in Ireland, your advice and foresight on the darkest days and there have been many, has kept me invested here and for the first time in my life it looks that I can retire financially secure...many thanks.

Irshpaddy ...I expect the share buyback to go through . As regards UK regulators concerns ,a simple search would have shown you the following Here are some key points on how UK regulators view share repurchases:

Market Abuse Regulations: The FCA regulates share buybacks under the Market Abuse Regulation (MAR). MAR sets out rules to prevent market manipulation and insider dealing, which includes rules governing share repurchases. Companies must ensure compliance with these regulations to avoid legal issues. Disclosure Requirements: Companies engaging in share buybacks must disclose the details of these transactions to the market. This includes the number of shares repurchased, the price paid, and the total value of the buyback. This information helps investors and regulators assess the company's financial health and management's decisions. Board Approval and Shareholder Communication: Share buybacks typically require approval from the company's board of directors and may also need shareholder approval in certain circumstances. Regulators emphasize the importance of clear communication with shareholders regarding the rationale behind the buyback and its potential impact on the company's financial position. Market Integrity and Fairness: Regulators are concerned about maintaining market integrity and fairness. They monitor share buybacks to ensure they are not used to manipulate the company's stock price artificially or to mislead investors. Companies must adhere to strict guidelines to prevent such abuses. Financial Stability and Capital Allocation: Regulators also consider the broader implications of share buybacks on financial stability and capital allocation. Excessive buybacks that jeopardize a company's ability to meet its financial obligations or invest in long-term growth may attract regulatory scrutiny. Overall, while UK regulators recognize the legitimate use of share buybacks as part of a company's capital management strategy, they enforce rules and guidelines to ensure transparency, fairness, and compliance with market regulations. Companies engaging in share repurchases must navigate these regulatory requirements carefully to avoid legal and reputational risks. User What is the difference between UK regulators and US regulators on share buybacks

ChatGPT The difference between UK regulators and US regulators regarding share buybacks primarily lies in the specific regulations, guidelines, and market dynamics of each jurisdiction. Here are some key differences:

Regulatory Bodies: UK: In the UK, the Financial Conduct Authority (FCA) oversees share buybacks under the Market Abuse Regulation (MAR) and other relevant guidelines. The London Stock Exchange (LSE) also plays a role in regulating companies listed on its exchange. US: In the US, share buybacks are regulated by the Securities and Exchange Commission (SEC). The SEC enforces rules and disclosure requirements related to buybacks, including those outlined in Regulation S-K and Regulation M. Regulatory Framework: UK: The UK's regulatory framework emphasizes transparency, fair dealing, and preventing market abuse. Companies must comply with disclosure requirements and ensure that buybacks are conducted in a manner that does not manipulate the market or mislead investors. US: The US regulatory framework for share buybacks also emphasizes transparency and fair dealing. However, there are specific rules governing the timing, pricing, and disclosure of buybacks, such as restrictions on buybacks during certain periods (e.g., blackout periods) and requirements for filing Form 10-Q or 10-K with the SEC. Legal Environment: UK: The legal environment in the UK may have different considerations regarding corporate governance, shareholder rights, and fiduciary duties compared to the US. Shareholder activism and engagement are also factors that influence how companies approach buybacks and how regulators view these activities. US: In the US, shareholder activism and corporate governance practices can impact the way companies conduct share buybacks. Proxy advisory firms and institutional investors often play a significant role in shaping shareholder resolutions and governance policies related to buybacks. Market Dynamics: UK: The UK stock market has its unique characteristics, including the presence of the London Stock Exchange and the regulatory landscape specific to the region. Market conditions, investor sentiment, and economic factors influence the frequency and scale of share buybacks in the UK. US: The US stock market is one of the largest and most liquid in the world, with diverse market participants and regulatory considerations. Buyback activities in the US market can have a significant impact on stock prices, market liquidity, and investor confidence. Overall, while both UK and US regulators aim to ensure fairness, transparency, and market integrity in share buybacks, the specific regulatory frameworks, legal environments, and market dynamics in each jurisdiction result in differences in how these activities are regulated and perceived. Companies operating in both regions must navigate the relevant regulatory requirements and market expectations when engaging in share buybacks. User Are UK regulators concerned about share buybacks for the purpose of inflating low priced shares

Yes, UK regulators are concerned about share buybacks being used for the purpose of inflating low-priced shares. This concern is rooted in the broader objective of preventing market manipulation and maintaining market integrity. Here are some key points regarding this concern:

Market Manipulation: Share buybacks can potentially be used as a tool for market manipulation, especially when they are used to artificially inflate the price of low-priced shares. This can mislead investors and create an inaccurate perception of the company's financial health or market value. Regulatory Oversight: The Financial Conduct Authority (FCA) in the UK closely monitors share buybacks under the Market Abuse Regulation (MAR) to ensure that they are not used for manipulative purposes. MAR sets out rules and guidelines to prevent market abuse, including activities like price manipulation through share buybacks. Disclosure Requirements: Companies engaging in share buybacks are required to disclose detailed information about these transactions to the market, including the number of shares repurchased, the price paid, and the total value of the buyback. This transparency helps regulators and investors assess the legitimacy of buyback activities. Fair Dealing and Investor Protection: UK regulators emphasize fair dealing and investor protection in the context of share buybacks. Companies must conduct buybacks in a manner that does not mislead or harm investors, including avoiding actions that artificially inflate share prices for short-term gains. Corporate Governance: Share buybacks are subject to scrutiny from a corporate governance perspective as well. Boards of directors and shareholders expect companies to use buybacks responsibly and in the best interests of shareholders and the long-term sustainability of the company. Overall, while share buybacks are a legitimate financial tool for companies, UK regulators are vigilant about ensuring that they are not used to manipulate markets, inflate share prices artificially, or mislead investors. Companies must adhere to regulatory requirements, transparency standards, and ethical practices when engaging in share buybacks to avoid regulatory scrutiny and maintain market confidence. User What are the UK regulators and banks concerns about share buybacks

UK regulators and banks have various concerns about share buybacks, which revolve around financial stability, market integrity, investor protection, and corporate governance. Here are some of the key concerns they may have:

Financial Stability: One of the primary concerns is that excessive share buybacks could impact a company's financial stability. If a company allocates too much capital to buybacks instead of investing in long-term growth, it may weaken its financial position, particularly during economic downturns or when faced with unexpected challenges. Market Manipulation: Regulators are concerned about the potential for share buybacks to be used for market manipulation. This includes artificially inflating share prices or creating misleading perceptions about a company's financial health or prospects. Such manipulation can harm investors and undermine market integrity. Liquidity and Capital Adequacy: Banks and regulators also consider the impact of share buybacks on a company's liquidity and capital adequacy. Excessive buybacks can reduce a company's cash reserves and available capital, which may affect its ability to meet financial obligations or pursue strategic initiatives. Investor Protection: Ensuring that investors are protected and well-informed is a key concern. Regulators require companies to disclose details of share buybacks, including the rationale, timing, pricing, and impact on capital structure. This transparency helps investors make informed decisions and assess the company's financial health. Corporate Governance: Share buybacks are scrutinized from a corporate governance perspective. Regulators and stakeholders expect boards of directors to act in the best interests of shareholders and the company as a whole. This includes evaluating whether share buybacks are an appropriate use of capital and align with long-term strategic objectives. Impact on Shareholder Returns: While share buybacks can enhance shareholder returns by reducing the number of shares outstanding, regulators and banks are concerned about the sustainability and effectiveness of buyback programs. They may assess whether buybacks are generating long-term value for shareholders or merely boosting short-term stock prices. Regulatory Compliance: Companies engaging in share buybacks must comply with regulatory requirements, including those related to market abuse, disclosure, insider trading, and corporate governance. Non-compliance can lead to legal and reputational risks. Overall, UK regulators and banks aim to strike a balance between allowing companies to use share buybacks as a legitimate capital management tool while ensuring that such activities are conducted responsibly, transparently, and in the best interests of shareholders and the broader financial system.

A simple, but critical question for Holt to answer at the upcoming 5/1/24 C.C....Is Amarin (or a successor Pharma Co. which buys Amarin) committed or NOT committed,by the Amarin 2018 collaboration agreement with Mochida...to pay milestone or royalty fees to Mochida for its patented product, LR-Et-EPA sales in the U.S. or in Europe?

IMHO everything else that Holt discusses at this conference pales in importance as compared with this question...Unless some unexpected bombshell announcement is released.

Zip….as another longtime holder, I agree…this company has been looking for a big pharma buyer for at least 10 years…BP knows the Patent wall didn’t hold up in the U.S. and likely has the same concern about EU…need a new EPA based product…

Nice find DMC..... I doubt Kiwi will believe this of course because the purity level of the oxygen some of the patients were breathing may or may not have been placebo controlled

TalShu, Outstanding reply to my post. What I found most interesting is how entrenched Novo Nordisk is in China. Of course, Europe is the most important market for a potential acquirer. China is an enigma. However, if an acquirer of AMRN (mainly for what they could do with Vazkepa in Europe) also had a way to optimize (or should I say to help Eddingpharm optimize) the uptake of Vascepa in China, that could be a real bonus. Of course, once China approves Vascepa for CVD that would be major step forward. If Eddingpharm were to work with a BP owner of AMRN that could provide greater distribution & other support (maybe with IP) that could be a win-win. Thanks again for well thought out and carefully documented comments!

Tal..." Holt’s narrative is the BOD’s focus on immediate, short-term, execution. To put it in his words: “the focus in the immediate term is really on executing what we have in our hands.”

i.e. In plain English Holt seems to be saying...Do what we can now to get the stock price up..and the sell the company and let the buyer take over and do the rest...e.g. developing LR-Et-EPA...This seems like a risk averse strategy that I'm not sure I'm happy with...Its a little disappointing...It isn't why I got into Amarin over 14 years ago

I could have bought Pfizer instead and benefited from a nice dividend all these years.

News

News  Market Data

Market Data  Discover

Discover